As kids we would have read the famous story of Alice in wonderland. In the story, she once reaches a crossroads and was not sure which road to take. A passing cat asked her where she wanted to go to which Alice replied

“I don’t know!”. The cat then smilingly replied “Then it doesn’t matter which road you take”.

The classic moment in the story is true to each of us in our daily lives. In our lives too we are often at crossroads like Alice and unknowingly we choose our roads without knowing where we want to reach in our life. When it comes to investments, this is in fact the reality for most of us. Since we don’t know what we want to achieve from our investments, any investment decision helps us achieve it.

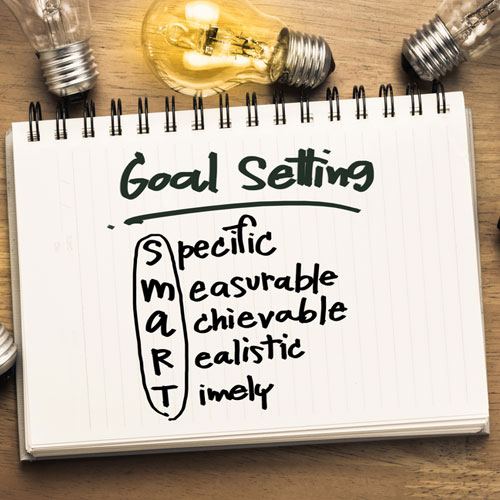

The need for setting goals can never be undermined, be it business, personal life or your personal finance. Every wise investor would know the purpose or objective behind his/her investments and more often than not, the same would be geared towards achievement of some goal in life. The goal can be any personal or financial goal like retirement or a fixed amount at any time in future, with the condition that it can be monetised or spoken in terms of money.

Advantage of setting goals:

The following are some of the benefits of setting financial goals in your life…

- Goals make you think & prioritise: When you actually start planning for your goals, you are forced to evaluate the need, intensity and priority for each of your goal in life. This gives you a lot of clarity on which goals to pursue and in what priority. Often important goals which are not on the top of your mind, crop up and make you think.

- Goals make you take action: After identifying goals, one becomes more inclined to take actions for achieving the goals. We often neglect or delay the action because the goals are not very clear in our minds. Defining goals would help you realise the urgency for taking appropriate actions

- Goals tells you where you: Unless the goals are defined, we would not be able to comprehend our current situation with regards to the future. Defining goals also clarify their feasibility and practicality for achievement and accordingly, depending of our current situation, we may either change the maturity period or the returns expectations or the targets of the goals.

- Goals helps you to keep focus: Understanding your goals would help us keep focus on achieving them. This helps us on a daily basis and you may start making a choice between making small expenditures or saving for the goals. Also, we would be more discipled and regular in making our investments and at the same time, not withdrawing from the kitty saved towards the goal.

- Goals lead to success: With goals in mind, you will make optimum use of your financial resources when while planning for them. You would eliminate wastefull expenditure, invest in productive asset classes and tend to maintain discipline in your investments. All these factors ensure that you are much closer to your goals then they mature.

Risks of not setting goals:

Just like we discussed the benefits of goal-setting, there are similarly down-side risks to not setting and planning for goals.

- Compromise on goals: Not identifying or delaying planning for your goals for too long would ultimately lead to situations wherein you would need to either compromise on your goals, in terms of value or by pushing our goals into future. However, more often than not, goals like child marriage, education, retirement, cannot be postponed and it is best left unsaid as to how you would plan when they actually arise. You may even loose out on smaller goals & moments of happiness like say vacations, which would be very much possible if you are planning in advance for them.

- Failure to make optimum use of finances: Not setting goals and planning for same will lead to misdirected investments and spendings. Chances are that there would be unwarranted spending which would had been invested had planning been done. There is also high chances that you would save in asset classes or product which are not in line with your goals. For e.g., While planning for retirement after say 15-20 years, you will probably identify equity as ideal asset class for you to invest. However, in absence of same, you may avoid equity investing as a risky asset since your goal & time horizon is not clear.

- Compromising on Long-term financial well-being: In long term, better management of your resources would enable you to achieve same while also creating and protecting your wealth at the same time. Needless to say, you are more likely to be credit-free, while having appropriate wealth at disposal for a better life, especially post retirement. By avoiding goal setting & planning, you may well be inviting financial in-stability or insecurity in long-run since you may be forced to take credit or dilute your unplanned investments when your goals mature.

Setting financial goals is something that we are not completely unaware of. It is like basic common-sense. We all know its importance but rarely do we plan and act accordingly. We have discussed in detail the benefits and risks of not setting your goals and planning for them. Very clearly, they have potentially very far-reaching & defining consequences to your financial well-being in future. Those who are wise would understand its criticality and start taking appropriate actions towards it in immediate future. And for those who fail to do would leave matters increasingly to luck and chance for as long as they continue delaying same.